Author Chris Asgill

Head of Steel View profile

The USA is a key supplier and consumer of cold metallics. If Section 232 is used to protect the US steel industry, EAF-based steel margins elsewhere will be compressed and steel producers will again need to turned to billet imports. This time, however, relief on margins from using imported billet is expected to be lower. Higher steel prices in the USA will not mean higher steel prices elsewhere, so margins will remain compressed, whether steel is produced via imported billet or imported scrap.

Section 232 will lift metallics prices, hurting steel margins outside the USA

The US has set itself on a collision course with steel trading partners, as the country’s administration looks for an easy win by protecting the domestic steel industry from imports to ‘make steel great again’. Josh Spoores has set out CRU’s view on the expected impact of Section 232 on steel prices here. For metallics, we believe that scrap prices internationally will rise as a result of any action on steel imports in the USA and that billet imports may not offer the same degree of relief as in 2014 and 2015. Outside the US there are both winners and losers of such a scenario, but EAF-based producers of both flat and long steel products will suffer the most.

While we do not expect that Section 232 will include US imports of steelmaking raw materials, not least because imports of pig iron and DRI are vital for the local industry, there are broader implications to consider. The USA is a key global consumer of these metallics and is also a key exporter of steel scrap. Through these, the US market has a significant influence on ferrous metallics prices.

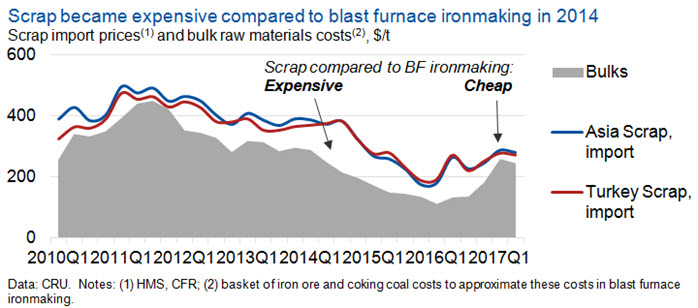

A case in point is 2014, when the US steel markets began to significantly outperforming other regional markets, one cause of which was protectionist measures, and this increased metallics demand. As a result, ferrous metallics prices lifted and they remained high compared with bulk raw materials (i.e. iron ore and coking coals) for much of the year. This hurt steel margins of EAF-based producers throughout Asia, Turkey, the Middle East and Africa that had to compete with more cost competive, BF/BOF-based material.

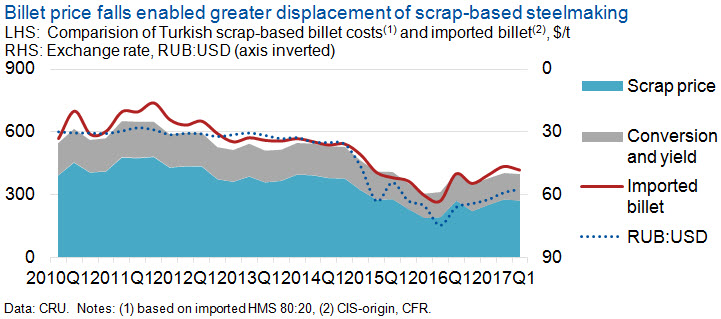

The catalyst for the subsequent collapse in ferrous metallics prices was multi-faceted, but one key driver was a fall in US steel output and, consequently, metallics demand. This combined with steelmakers elsewhere reducing their own steel make and turning instead to cheaper imported billet. Billet exports from China rose sharply from 2014 Q3, particularly to Asia, which was hardest hit due to the combination of high scrap prices and lower finished steel prices. By early 2015, billet exports were rising the CIS, following currency devaluations in Russia and Ukraine. By late 2015, despite scrap prices having fallen back compared to bulk raw materials, Chinese exports of billet continued to surge as the domestic market there weakened and by 2015 Q4 Chinese steelmakers were facing some of the worst conditions in recent history.

Back to the future…

While the current Section 232 investigation relates directly to steel products only, we expect the impact will be to lift prices across the whole steel value chain in the country. That is, on the assumption that the USA is looking to return imports to the levels exhibited in 2010 and 2011, this suggests 0.6-0.8 Mt/m less import material available (i.e. over 7 Mt annualised) compared with today that will, certainly, lift steel prices.

Higher steel prices will encourage greater domestic production of steel and this will lift both domestic demand and prices for all raw materials. However, given the structure of the different raw material markets, at the global level, we anticipate that cold metallics will be impacted to a much greater degree than iron ore and coking coal.

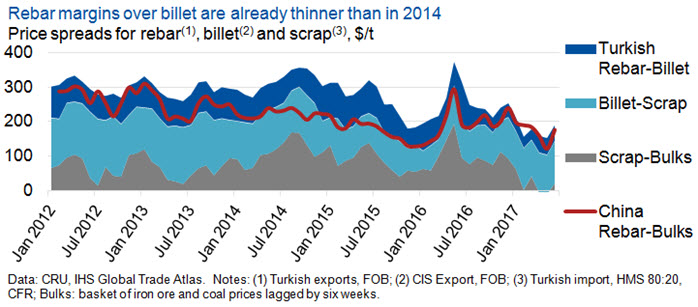

Although in 2014 and 2015 steelmakers were able to turn to billet in the face of higher scrap scrap, this time we expect that billet offers will be less forthcoming, particularly at the highly competitive levels compared to scrap back then. This is because the benefits of sharp currency depreciations have waned, through domestic cost inflation, and utilisation of assets is set to rise, even with our base case outlook (i.e. without the impact of Section 232) for falling billet exports. Furthermore, margins on steel products over both billet and scrap are much tighter today than they were in 2014 and 2015.

In the event of higher metallics prices, we do expect imported billet to displace some EAF-based steelmaking again, as per 2014 and 2015. However, there will be little room for international metallics prices to remain at current lower levels, despite lower demand levels. Unlike 2014, international scrap prices are now largely in line with those in the USA. With the US market continuing to act as a price floor for international prices, there is little flexibility for global makets not to rise in line with the US market. Furthermore, a key catalyst for the correction in US, and indeed international, scrap prices was a fall in demand in key scrap supply markets, notably the US and Europe. Broad action on steel imports in the USA would lift scrap demand in a more sustained fashion than previously. All-in-all, EAF-based steel margins outside the USA are expected to remain narrow, potentially narrowing further.

Explore this topic with CRU

Author Chris Asgill

Head of Steel View profileThe Latest from CRU

China’s phosphate sector proves resilient amid overzealous LFP output

China dominates the supply and consumption of LxFP cathode active material (CAM) and has invested heavily in capacity. However, this has now resulted in the production of...