Steel mills importing into Europe based in India, Vietnam and Ukraine will be the most disadvantaged under CBAM. This will lead to a change in trade flows. However, given Europe will be increasingly import dependent, imports from these countries will not be wholly displaced and EU prices will have to rise exceptionally to incentivise imports from these countries. This should lift the profitability and capacity utilisation of EU mills.

Having said that, the full impact of CBAM will only be apparent in 2034 when free allowances are eliminated to create a truly ‘level playing field’, but only for sales within Europe. Until then, EU mills will remain disadvantaged relative to importers in the EU market. Additionally, EU mills will remain disadvantaged in the export market regardless of CBAM. As a result, survivability will be an issue for some.

In this insight, we use the CBAM module in CRU’s Steel Cost Model to determine the impact of CBAM charging on the costs of individual steel mills outside Europe to understand how the shares of imports into Europe and, importantly, steel pricing might be impacted.

CBAM will lift steel prices as EU import dependence increases

From 1 October, the EU required importers of products covered by CBAM (e.g. steel, cement, ferroalloys etc.) to begin reporting data on their emissions. This initial phase only requires data to be reported and is intended to build capacity, allow fine tuning of the reporting system and to better understand potential impacts of CBAM. However, from 1 January 2026, importers will need to surrender purchased emission allowances (EUA) to cover chargeable emissions over and above notional free allowances on all imports. These costs will grow over time as notional free allowances are eliminated and carbon prices rise.

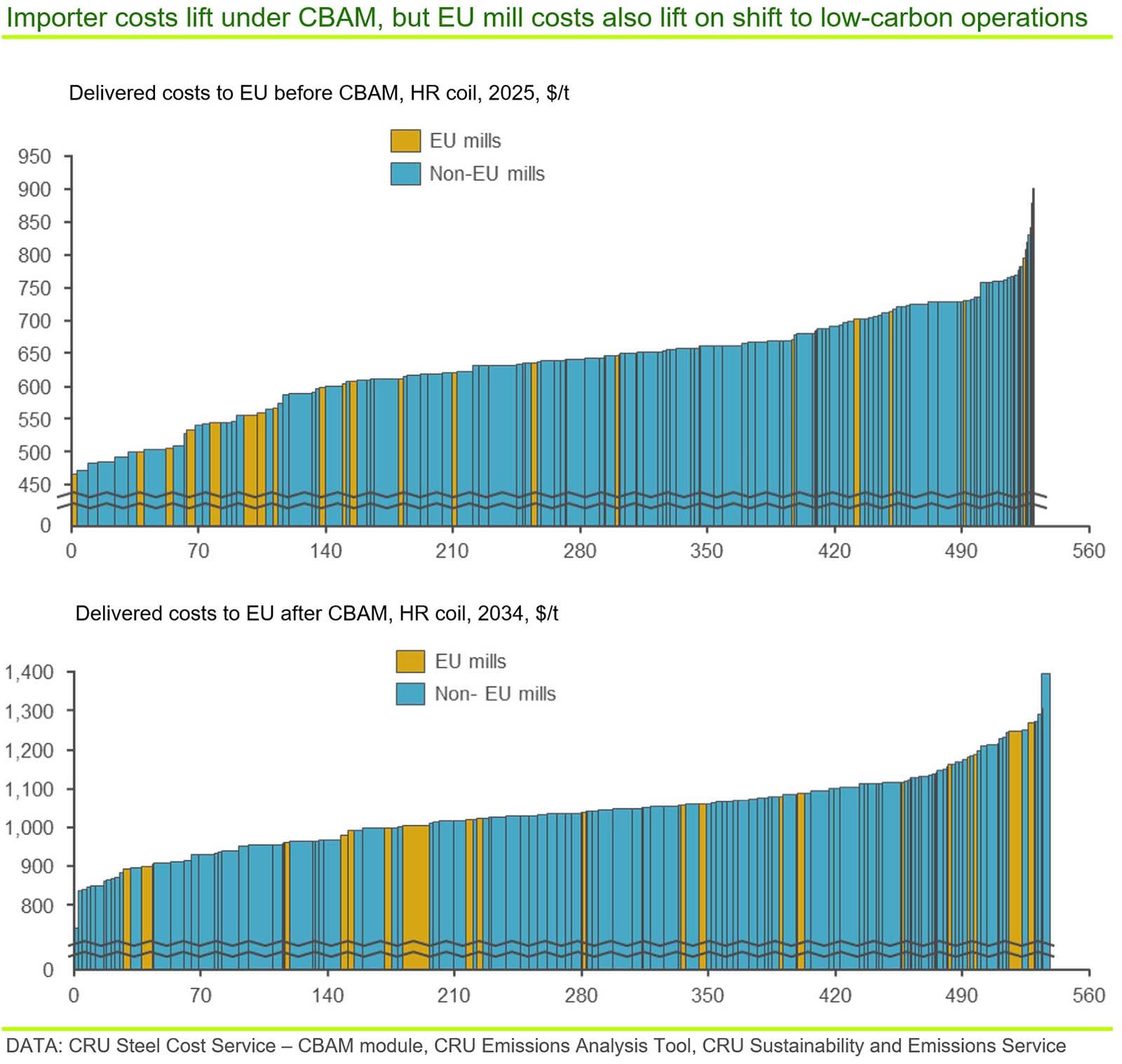

The following two charts show the global ‘Europe delivered’ cost curve for Hot Rolled (HR) coil including full production from all mills covered by CRU’s Steel Cost Model, whether currently importers of steel into Europe or not. The first chart shows the delivered cost curve prior to implementation of CBAM, the second, the expected position in 2034 when free allowances have been eliminated and carbon prices have lifted. Underlying raw material and other costs will reflect CRU forecasts in each year.

These curves show the degree to which CBAM will raise importers’ costs. Interestingly, European mills do not gain relative to importers as CBAM is implemented (n.b. in fact, EU mills appear to move to the right on the curve), largely as costs in Europe are also rising exceptionally due to the implementation of higher cost, low carbon operations. Essentially, this effect demonstrates the CO2 price forecast for 2034 is not yet sufficiently high to offset the added cost of low-carbon steelmaking.

The underlying data also shows that importing mills move position within the curve between the years, indicating changes in cost competitiveness relative to other importers. These changes will be relevant for both trade flows and – given Europe will be increasingly import dependent – steel prices in Europe, which will need to rise to incentivise imports regardless of who is importing.

Not shown here is that EU mills will be increasingly disadvantaged in their export markets as all EU production is charged for carbon emissions regardless of whether it is sold into Europe or not, whereas mills outside Europe are not charged on steel sold outside Europe.

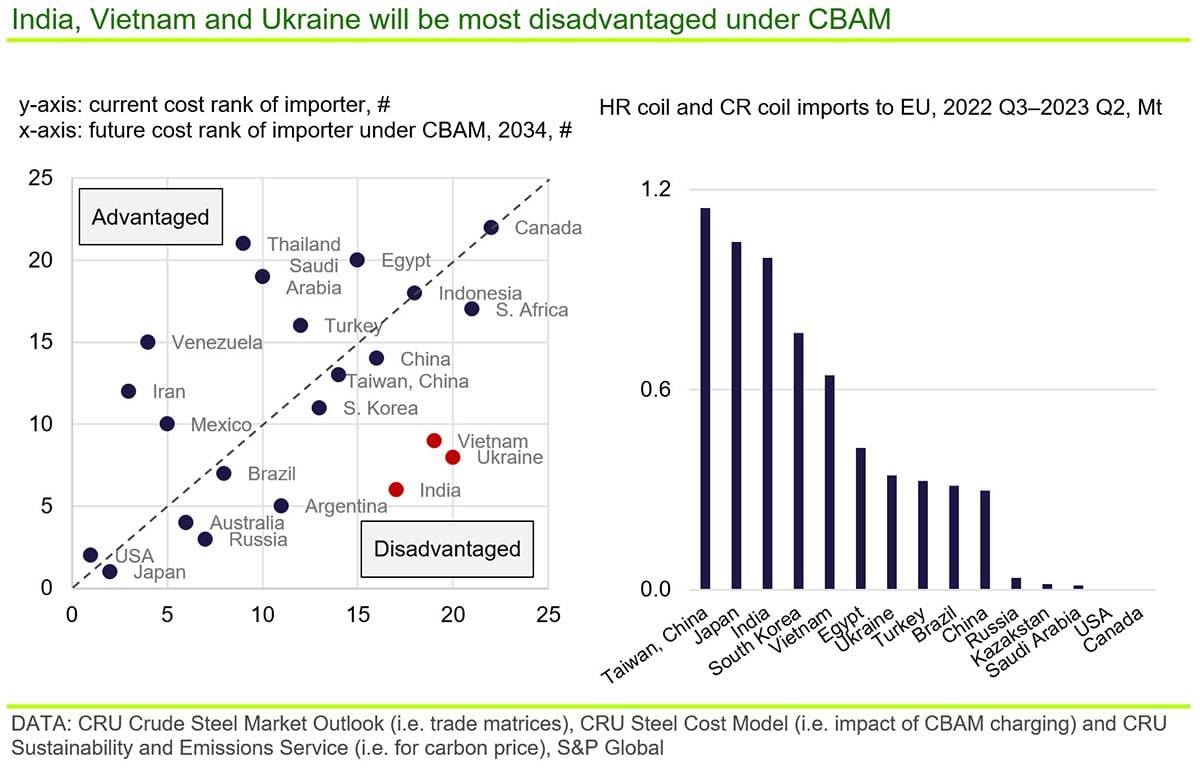

India the big loser under CBAM, but will remain an importer

To better understand which mills gain and which lose, the left hand chart below shows changes to the ranking of import countries on the cost curve under CBAM, using weighted average CBAM costs on a mill-by-mill basis. Amongst the Top 10 importers into Europe, India, Vietnam and Ukraine will be particularly disadvantaged by CBAM; Thailand, Saudi Arabia, Venezuela and Iran will be advantaged; whereas China, Taiwan (China), Japan, South Korea and Brazil will remain similarly positioned.

Given mills in India, Vietnam and Ukraine account for ~30% of HR coil and CR coil imports into Europe, this is likely to lead to changing trade flows. However, the degree to which import volumes switch will depend on several factors, such as availability of supply, relative pricing in domestic markets, quality constraints etc. (n.b. Ukraine imports are already affected by the war; further impacts due to the war are not specifically considered here).

For example, the USA is not a major importer into Europe today, but its competitive position versus current importers will improve under CBAM, opening opportunities to displace those imports. The chart below shows the competitiveness of US mills will improve by ~$230 /t versus India, Vietnam and Ukraine (e.g. ~$412 /t cost uplift – the arithmetic mean for India, Vietnam and Ukraine – minus $183 /t). That is, assuming mills in these latter countries remain price setters in the European market, US mills should see an uplift in profitability of ~$230 /t on sales to Europe. However, this uplift may not be sufficient to incentivise exports from the USA to Europe unless it outweighs the sum of delivery costs from the USA to Europe plus any domestic price premium available to US mills. Under current delivery costs and price premia, this would not be the case and the situation would be less advantageous if domestic price premia are lifted further by a US carbon border charge, which is a possibility. As such, we would not expect US mills to start exporting to Europe under these conditions.

More generally, given CRU’s forecast that imports into Europe will increase over time, it is far from certain that higher cost imports from India, Vietnam and Ukraine will, or can, be wholly displaced. Under this situation, steel from these countries will still be needed and European prices will need to rise to incentivise these imports. An interesting knock-on effect of this is that steel prices in Europe will become closely linked to the level of decarbonisation – and, therefore, level of carbon charge under CBAM – achieved by exporting mills in, for example, India.

EU mill capacity utilisation will rise; but output depends on surviving capacity

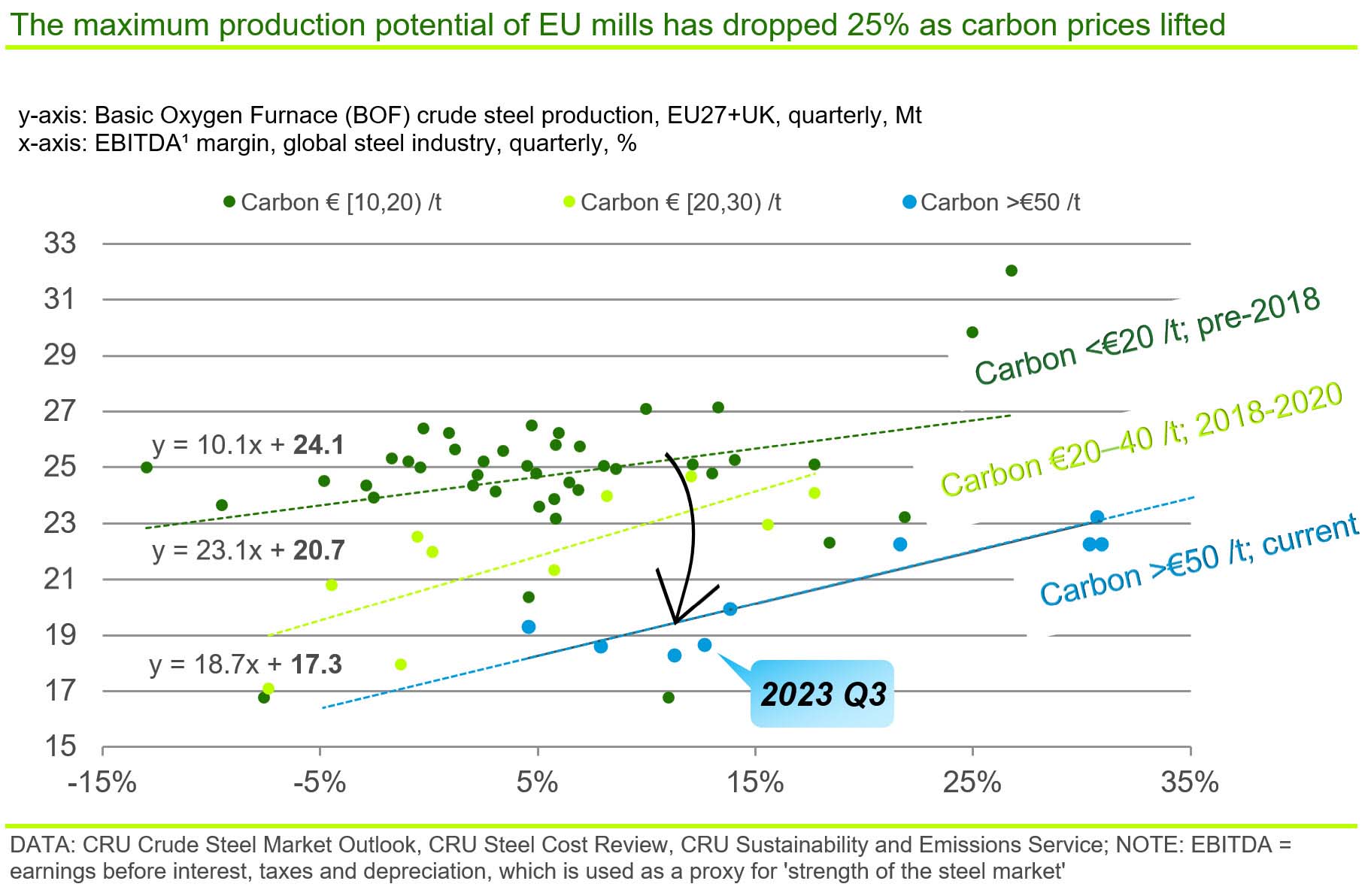

EU mills have clearly been disadvantaged by carbon charging and, as a result, the maximum production potential of the industry has fallen by ~25% in the last few years as carbon prices lifted above ~€50 /t. That is, economically accessible markets have eroded due to more competitively costed imports (see chart).

CBAM is intended to reverse this disadvantage but there will not be a truly ‘level playing field’ for sales within the EU market until all free allowances are removed – only by 2034 – when importers will be charged the full carbon cost. Before then, EU mill marginal costs will remain far above those of importers and EU mills will remain uncompetitive in those market segments competing with imports. Additionally, there will never be a ‘level playing field’ for sales outside of Europe – CBAM does not address this at all – and EU mills will be increasingly disadvantaged in export markets as carbon prices rise.

Once free allowances are removed, the difference in carbon cost between EU mills and importers effectively reverts to zero for sales within Europe. In the above chart, this is equivalent to the EU industry moving back towards the upper relationship (i.e. dark green data points), implying up to ~30% uplift in maximum production potential relative to today. However, the increasing loss of competitiveness in export markets means EU mills are unlikely to return fully to that level of production.

Thus, importing mills will see higher costs due to CBAM and European steel prices will have to rise to incentivise these imports. Higher prices will widen the scope for EU mills to invest in decarbonisation technologies, but there will never be true cost parity with importers as EU mills will always be disadvantaged in export markets. As such, the European industry is not expected to recover its historical maximum production potential, which could have implications for survivability of some mills.

If you are interested in understanding how CBAM will influence import trade and steel pricing in the EU or how CRU’s Steel Cost Model and CBAM module can help you, please get in touch, we’ll be happy to talk.