This snapshot overview provides a quick glance at the anticipated shifts within the aluminium industry for 2024, reflecting the impact of global economic, geopolitical, and environmental trends. The focus areas include China's growing scrap demand, the upward trend in bauxite prices, the evolving carbon products landscape, and fluctuations in LME prices. As the industry faces these developments, stakeholders are gearing up to address the resulting opportunities and challenges.

In a concise overview, we present CRU's top ten predictions for the aluminium sector in 2024. These forecasts touch on pivotal aspects like market demand, regulatory shifts, and sustainability initiatives. For those navigating the aluminium market, this brief offers essential insights into what to expect in the upcoming year, without delving into detailed analysis.

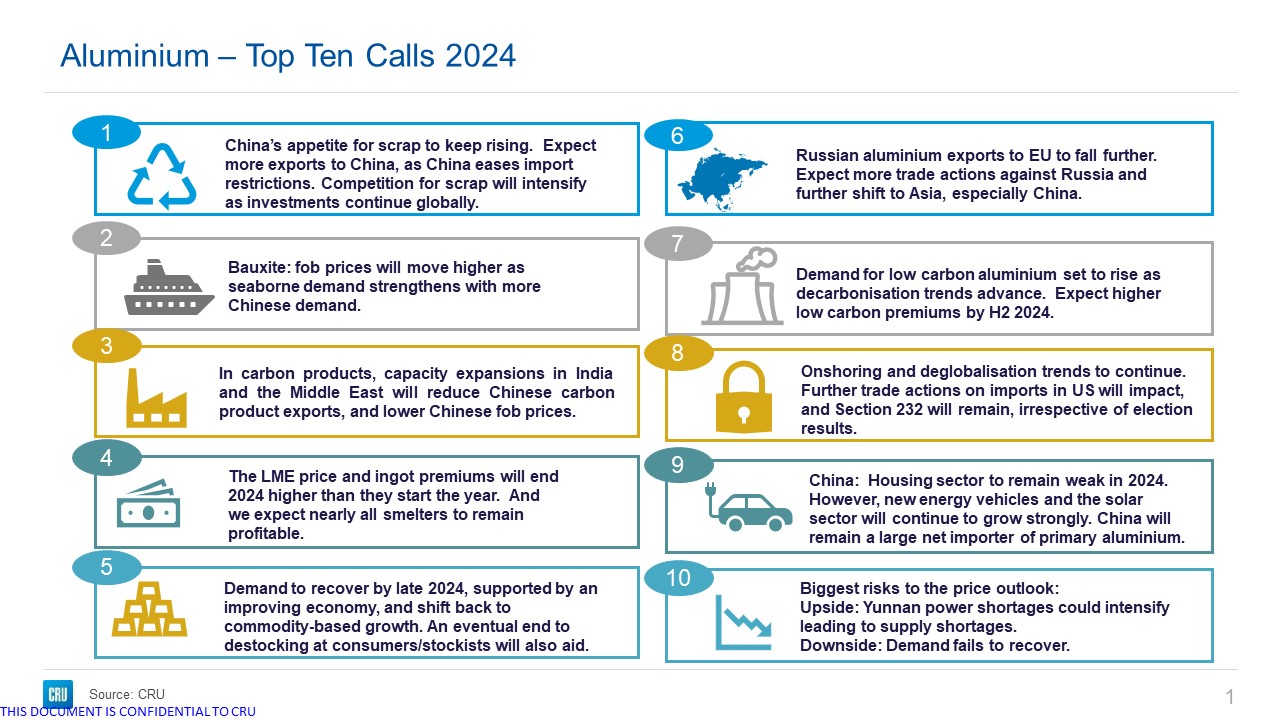

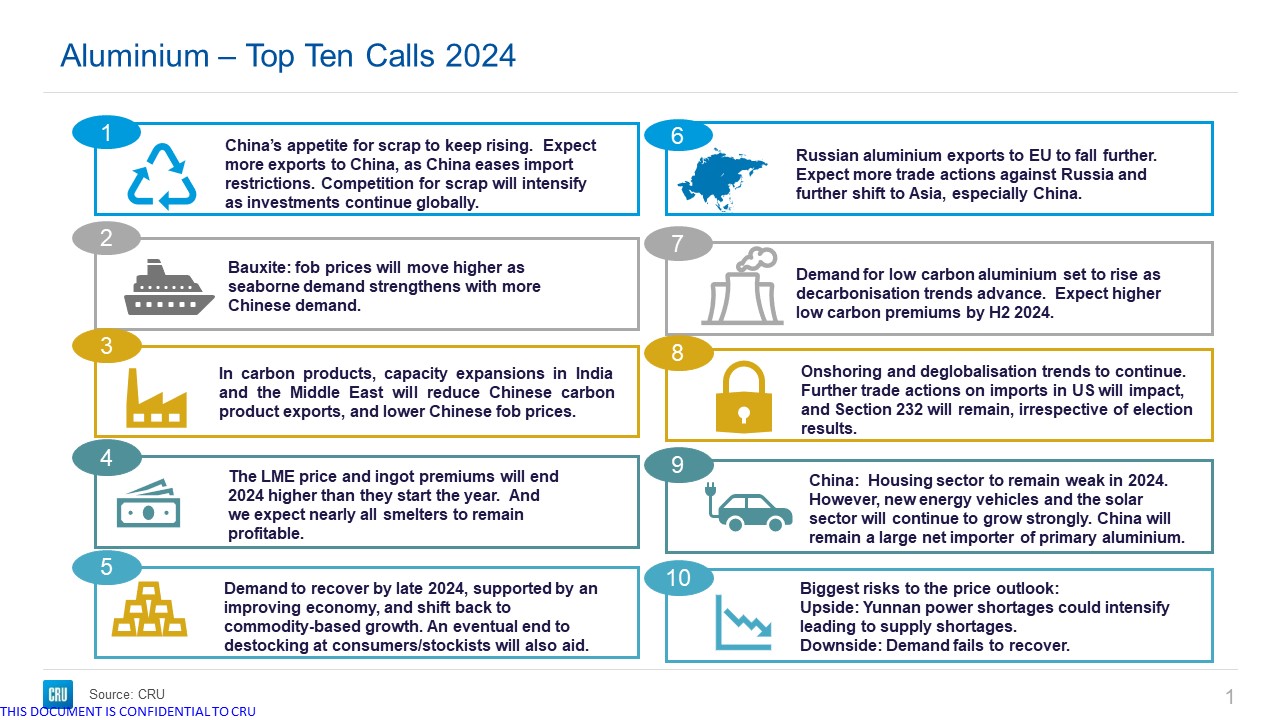

1. Rising Scrap Demand in China

China’s appetite for scrap keeps rising. Expect more exports to China, as China eases import restrictions. Competition for scrap will intensify as investments continue globally.

2. Higher Bauxite Prices on Increased Chinese Demand

Bauxite: fob prices will move higher as seaborne demand strengthens with more Chinese demand.

3. Shift in Carbon Products Market Dynamics

In carbon products, capacity expansions in India and the Middle East will reduce Chinese carbon product exports, and lower Chinese fob prices.

4. LME Prices and Ingot Premiums to Increase

The London Metal Exchange price and ingot premiums will end 2024 higher than they started the year. And we expect nearly all smelters to remain profitable.

5. Economic Recovery Boosts Aluminium Demand

Demand to recover by late 2024, supported by an improving economy, and shift back to commodity-based growth. An eventual end to destocking at consumers/stockists will also aid.

Click here or below to enlarge the image

6. Decrease in Russian Aluminium Exports to EU

Russian aluminium exports to EU to fall further. Expect more trade actions against Russia and further shift to Asia, especially China.

7. Growing Demand for Low Carbon Aluminium

Demand for low carbon aluminium set to rise as decarbonisation trends advance. Expect higher low carbon premiums by H2 2024.

8. Onshoring and Deglobalisation Affecting Trade

Onshoring and deglobalisation trends to continue. Further trade actions on imports in US will impact, and Section 232 will remain, irrespective of election results.

9. China's Sector-Specific Aluminium Demand Trends

China: Housing sector to remain weak in 2024. However, new energy vehicles and the solar sector will continue to grow strongly. China will remain a large net importer of primary aluminium.

10. Key Risks to Aluminium Price Outlook

Biggest risks to the price outlook: Upside: Yunnan power shortages could intensify leading to supply shortages. Downside: Demand fails to recover.

Explore this topic with CRU