Despite excess smelting capacity and progressively tighter concentrate markets, we expect the Chinese smelting industry to continue growing during the next four years. In fact, there is potential for even higher growth rates than we currently expect in our base case scenario, due to the short lead times associated with the development of new smelter projects and changes in project status.

There are several reasons for this situation. First, there is room for China's cathode self-sufficiency rate to increase further. Even though China has been the biggest producer of copper cathodes in the world for several years, it still needs to import between 30-40% of its total cathode consumption every year, which means that government support, in the form of low-cost loans, environmental approval and access to land, among other, is readily available for smelters.

Second, the Chinese economy has been slowing down and producers from traditional industries like coal, steel, aluminium and cement have been struggling to survive, not to mention make a profit. In contrast, Chinese copper producers have remained profitable due to the high TC/RCs. According to the latest data from China Nonferrous Metals Industry Association (CNIA), profits obtained by Chinese copper smelters hit RMB 2.0B in Q1 2016, up 41.35% y-on-y. The high levels of concentrate imports to China registered during the first half of 2016 are a visible consequence of these profits.

Third, rising copper prices provide additional incentives to Chinese copper smelters. CRU is forecasting refined copper prices to reach the bottom of the cycle in 2017 and to start rebounding from 2018 onwards. Although TC/RCs are expected to fall over the same period, it should be noted that some Chinese smelters prefer a scenario of rising copper prices to one of rising TC/RCs when their copper concentrate purchases are not strictly hedged. In those cases, being exposed to an increasing copper price trend might be an opportunity for significant profits.

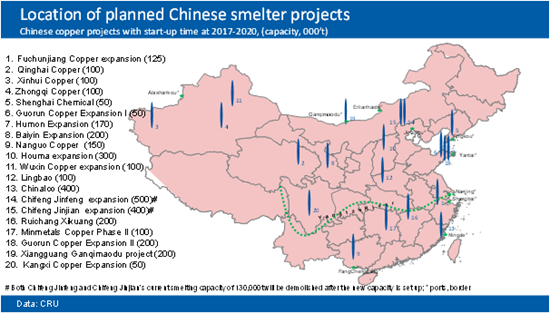

Fourth, the lead-time of Chinese copper smelting projects is very short. Over the past six months, we have added several new projects to our database, with a combined production capacity of more than 1Mt of blister. The projects are Chifeng Jinfeng's 500,000t/y expansion, Chifeng Jinjian's 400,000t/y expansion, Zhongqi Copper's 100,000t/y expansion, the 100,00t/y Lingbao smelting project, Shenghai Chemical's 50,000t/y expansion and Yantai Guorun's 50,000t/y expansion project. We cannot rule out the addition of other smelter projects, especially in consideration of the above-mentioned factors, that is, the government sponsored self-sufficiency drive, the profitability of the business at current TC/RCs and rising copper prices after 2017.

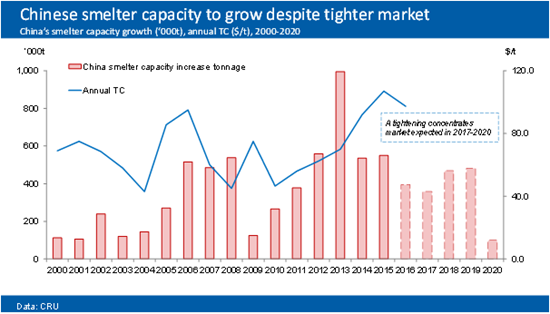

Over 70% of the increase in global smelter capacity during the next four years will take place in China. Thus, the development of China's smelter projects are an important factor for the global copper concentrates market balance and has drawn the attention of market participants. How, whether and when each of these projects might be commissioned has been of great interest to different parties.

Our view is that the potential for most of the planned projects to start operating might be higher than many in the market expect. To support this view, in the July issue of Copper Studies we conduct a detailed analysis of Chinese smelting capacity during the period of 2017 to 2020. We consider the location of each project, its transportation requirements and availability of raw materials; we also analyze the capex of these projects, as well as the technology and ownership of each of them; finally, we provide background information for each smelter project and our view on its development outlook.

Drawing on in-depth research produced by CRU's base metals team, Copper Studies provides a comprehensive analysis of issues relating to all aspects of the copper industry.

Explore this topic with CRUThe Latest from CRU

Key takeaways from CRU’s Wire and Cable Amsterdam conference

CRU held its seventeenth consecutive Wire and Cable conference in Amsterdam, during 24–26 June 2024. Day 1 kicked off with a warm welcome to around 200 conference...