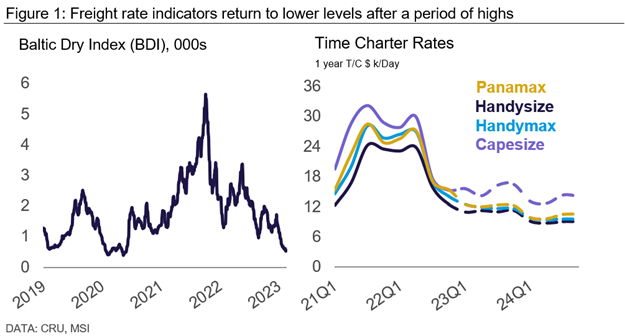

Freight rates have fallen sharply so far in 2023. After a golden time for the shipping industry, we have seen a progressive weakening of freight rates throughout the past year as congestion eased and global economic growth slowed. Shipping firms did not begin 2023 with much optimism. Prices continued to fall in early 2023, reflecting disruptions to commodity production caused by bad weather and the seasonal Chinese New Year slowdown. The Baltic Dry Index (BDI) decreased 56% from the beginning of January to 21 February to reach the lowest level in over two and a half years (Figure 1, right-hand side).

The decline in earnings across the market is notable. Time charter rates underline the current weakness of the market. A one-year time charter on a Capesize ship in 2022 Q1 would have earned owners $28,000 /day, whereas for 2023 Q1 the Maritime Forecasting and Strategic Advisory (MSI) forecasts $16,000 /day (Figure 1, left-hand side).

We expect a modest recovery in 2023 H2

The question now is whether rates are set to continue this downward trend. As weather problems fade and Chinese economic growth rises, demand should improve from the very weak levels in January and February. However, broader fundamentals do not look strong for 2023. Despite the global slowdown, MSI expects modest growth of 1.8% y/y in cargo volumes this year, following a steady trade outlook for iron ore and a positive outlook for minor bulks. Improved fleet efficiency will, however, translate this into a fall of 1% y/y in deadweight tonnage demand for dry bulk shipping. This means ships will carry more cargo tonnes per deadweight tonnage. At the same time, supply is expected to increase by 3% y/y. Although demolitions are set to grow from their low level in 2022, this year will bring another influx (~30 MDwt) of newly built ships. The net effect from fleet growth and deadweight tonnage demand reduction is a 32.5 MDwt increase in fleet supply.

Demand will partly depend on the nature of recovery in China. Previous surges in Chinese growth – for example after the 2008-09 financial crisis – have been driven by commodity-intensive investment spending. If this recovery is led by consumer spending, particularly on services, it will create less demand for dry bulk freight.

The outlook is rather conservative in the coming quarters. MSI forecasts modest improvements in average rates for the four dry bulk vessel segments towards 2023 H2 as temporary factors such as unfavourable weather fade. The Forward Freight Agreement (FFA) curve shows Capesize rates will improve in 2023 H2, standing as of market close at ~$18,625 /day for 2023 Q3 and $18,275 /day for 2023 Q4, up from $13,600 /day for 2023 Q2.Given the supply-demand fundamentals, however, there is little chance of a return to the high rates of 2021-22.

The container shipping sector outlook for 2023 does not look strong either. Fleet growth is expected to accelerate markedly. The orderbook of newbuild container ships, expected to be delivered between this year and 2027, is equivalent to about one-quarter of the existing carrying capacity, according to Drewry. A combination of sluggish demand and a sharp increase in vessel delivery will likely challenge the container freight market in 2023.

These and other economic developments that impact commodity markets are discussed with CRU subscribers regularly. To enquire about CRU services or to discuss this topic in detail, get in touch with us.

Explore this topic with CRU