AuthorAlex Tuckett

Head of Economics View profile

Co-AuthorPeter Ghilchik

Head of Multi Commodity Analysis View profile2021 will be a year of hope for recovery after the coronavirus pandemic left its mark on the world in 2020. Monitoring the speed and nature of the recovery will be vital to understanding all markets.

Drawing on conversations between market experts and people across commodity value chains, CRU expects interest in three topics to intensify and dominate the conversation in 2021: carbon emissions abatement, China’s 14th Five Year Plan, and how policy will reshape global trade.

CRU Macro themes

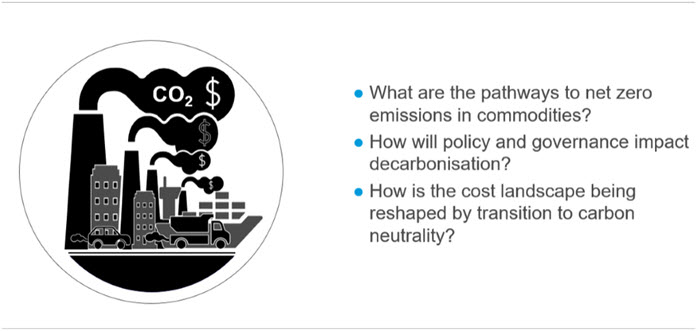

Carbon Emissions

The growth in renewables as the energy source for power, together with the electrification of mining equipment, is a key enabler for decarbonisation. New technologies, including: carbon capture, hydrogen as a fuel, process and supply chain optimisation, and recycling, will be important levers. Over the course of 2021, CRU will examine the implications of applying these approaches across value chains to optimise emissions abatement.

In 2021, governments will shift from rhetoric to policy implementation. The EU will announce details of its carbon border adjustment mechanisms (CBAM); China will provide details of decarbonisation priorities in its 14th Five Year Plan plan, and the US will re-join the Paris Agreement. How will other countries respond to increasing climate ambitions in these major economies? How will this impact trade flows and metal prices when implemented? How effective will climate policies be in supporting the uptake of EVs and the rise of recycling rates of end-of-life goods?

Emerging global carbon prices will escalate costs of high carbon emitters and alter value-in-use assessments. CRU’s analysis of costs will explain how this will tilt and re-shuffle global cost curves and reshape supply pipelines; we will highlight assets that are at risk of becoming stranded due to escalating costs; meanwhile, where downstream manufacturers who are increasingly demanding ‘green metal’ to meet sustainability targets – we will be assessing if low carbon products attract a premium.

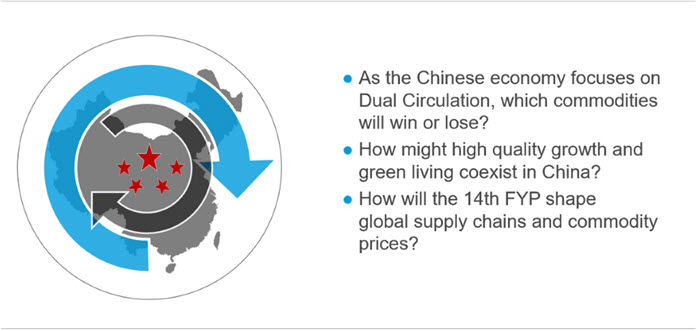

China Five Year Plan

2021 marks the launch of China’s 14th five-year plan (FYP). It will provide a roadmap through to 2025 and beyond. Markets will gain greater clarity about China’s Dual Circulation strategy. CRU will consider the emphasis the new FYP puts on internal circulation and domestic consumption as the main pillar of economic growth, as well as consider the pace at which China may pivot away from infrastructure investment and trade. We will look at how the country’s new growth and development targets feed through to metal end-use demand and commodity demand, and consider the commodity winners and losers.

China’s 14th FYP will see increased focus on green living and high-quality growth. The aspiration is to achieve this through greater self-reliance and technological innovation. Smarter use of investment and regional supply chains will allow Chinese industry to move up the value chain. China will also provide details of decarbonisation priorities in its next FYP. CRU will look at how high quality growth and green living might coexist in China, and consider the pace of investment slowdown in traditional forms of infrastructure (roads and buildings). We will assess what this means for commodity demand and look at which new technologies could be backed.

As part of the 14th FYP, China is looking to increase its self-reliance. Domestically produced metals are likely to gain. Overseas investment in mining and metal resources will continue to guarantee the supply of critical materials. Which strategic mining assets might China purchase next? Will it prefer to buy greenfield projects or M&A? CRU will seek to answer these questions and consider how these actions could result in displacement of countries that currently export commodities to China – and how these decisions affect global supply chains and commodity prices.

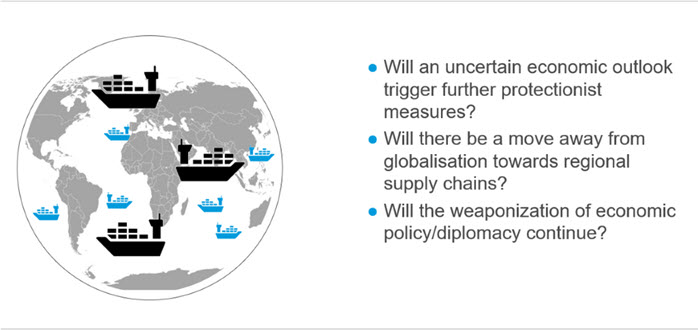

Reshaping Global Trade

The prevalence of regulatory trade protectionism has been increasing – and Covid-19 has exacerbated this trend. Will the rapid change in industry structure (decarbonisation), Covid-19 paranoia, and shifting attitudes to populism fortify or destroy commodity trade barriers?

Regionalisation was a trend before Covid-19 disrupted the world. But the pandemic has created more ‘noise’ around the diversification of global supply chains. CRU will consider the enforcement of trade barriers and whether they will encourage more supply chain regionalisation. And we will look at commodity trade flows and industry cost structures and how these may be affected.

Security and geo-political concerns have spilled over into trade and investment protectionism. Opposing sides have looked to ‘hit them where it hurts’ in key industries/commodities. Will 2021 bring an easing of tensions? Or will they continue to simmer and severely disrupt global commodity trade flows? CRU will seek to answer these questions and many others as the year progresses.

Explore this topic with CRUEconomic team

-

Veronika Akhmadieva

Senior Economist London -

Cristobal Arias

Senior Cost Analyst London -

Henry Hao

Principal Economist Singapore -

Glen Kurokawa

Power Sector Lead London -

Ilona Khachirova

Analyst London